Wages in North America

In 2024, wages grew in North America as the economy continued to grow at a higher pace relative to the rest of the world. Wages are likely to continue strong growth in 2025, as inflation is expected to rise again, but could be dampened by a continually weakening real economy.

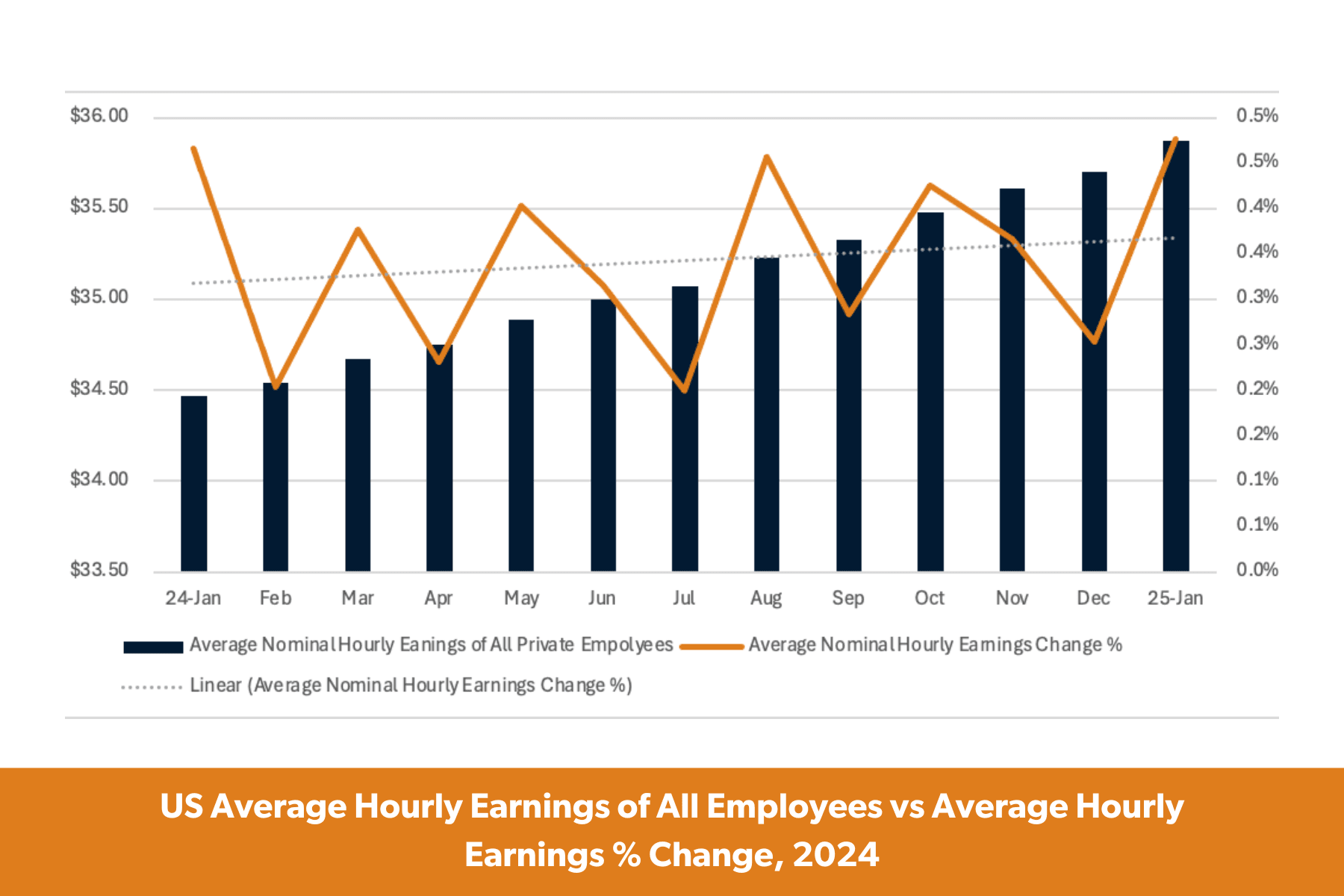

In 2024, US average hourly earnings grew nominally by $1.40, or 4.5%. This is a slight uptick from 2023, when average hourly earnings grew at 4.3%, and a return to the 4.5% average hourly earnings growth seen in 2022. The average hourly earnings growth in 2024 was driven by strong overall economic growth in the US and wages continuing to catch up to stabilizing prices. While the labor market was primarily driven by healthcare, education and government hiring in 2024, these sectors did not primarily drive wage growth.

The sectors that saw the most growth in average hourly earnings were professional and business services at 5.1%; other services (e.g., social assistance, emergency services, housing) at 4.7%; and information at 4.6%. Sectors that saw the least average hourly earnings growth include mining and logging at 2%, wholesale trade at 2.3%; and transportation and warehousing at 2.5%. These sectors lost jobs or hired minimally in 2024, leading to lower sectoral wages.

Regionally, wages have grown most in high-cost markets (e.g., San Francisco, New York, Boston), as these markets have high inflation and are home to the top-paying companies in the world. Wages in high-cost markets have grown 44% since 2019 and have continued to become increasingly untethered from the growth of medium- and low-cost markets.

Medium-cost (e.g., Chicago, Denver, Cleveland) and low-cost (e.g., Tampa, Oklahoma City) labor markets have not seen the same wage growth as high-cost markets. From 2019 to 2024, medium-cost markets have grown by 32%, while low-cost market wages have grown by 28%. Wage growth in these areas has been driven by employers hiring more in these markets as they look to lower overall labor costs. This trend is likely to continue to help drive wage growth in the coming years in these markets.

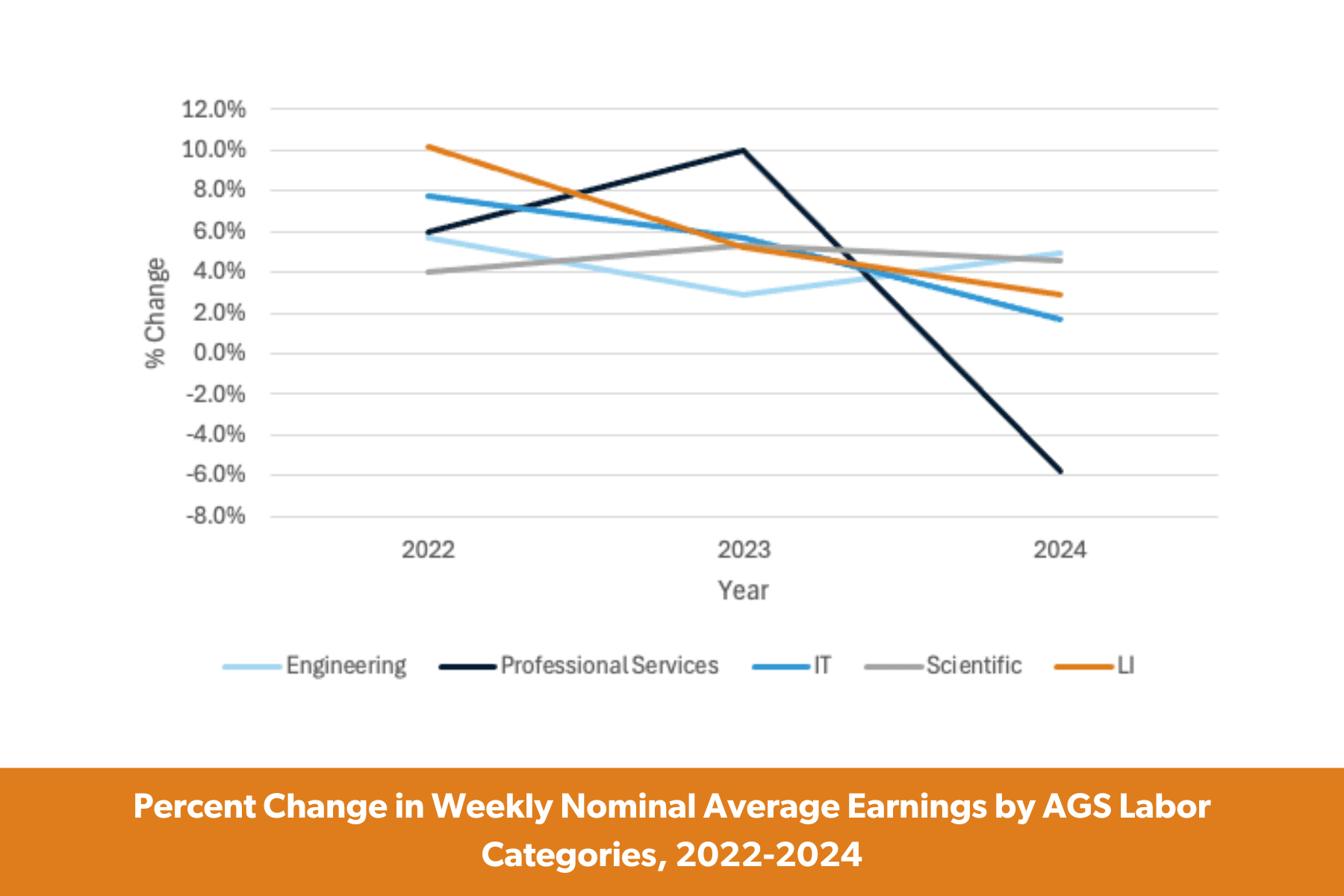

Looking at AGS labor categories, nationally, engineering jobs led median weekly nominal earnings growth in 2024, coming in at 4.9%. This was the only labor category to see higher wage growth than 2023, when earnings grew at 2.9%. This low earnings growth in 2023 led to a bounce back in wage growth in 2024. Earnings growth is also bolstered by a reduced number of engineering graduates and holes left in the workforce by retired engineers. Earnings may continue to climb in 2025, but tariffs and reduced manufacturing activity may lead to reduced growth.

Scientific/healthcare jobs experienced 4.5% weekly nominal earnings growth in 2024, down from 5.3% in 2023. Continually strong hiring in the healthcare sector drove wage growth in 2024, as the US continues to invest in care for an aging population and expansion for low-income populations. Earnings could continue to grow at a strong pace in 2025, but looming cuts to Medicaid and other social services bring that growth into question.

Median weekly nominal earnings for light industrial jobs grew at 2.9% over the course of 2024. Growth in weekly nominal earnings has fallen sharply for light industrial Jobs, down from 10.2% in 2022 and 5.2% in 2023. While worker shortages persist in the light industrial space, layoffs have been common in the sector. Manufacturing lost 87,000 jobs in 2024 even as the US Federal Government made significant investments into the sector. Continued layoffs, reduced manufacturing activity and tariffs have the potential to drag on light industrial wage growth in 2025.

IT weekly nominal earnings growth was down in 2024, at 1.6%. In 2022, earnings grew at 7.8%, followed by 5.6% in 2023. The tech sector overall has seen cooling over the past two years, except for AI, which still drives hiring in the space. Layoffs and slow hiring (minus AI) caused large variations in sectoral unemployment, with large differences in the available talent pool contributing to slow earnings growth. AI roles will continue to see higher wage growth in 2025, but as the overall labor market continues to slow, expect wages for more traditional roles to grow comparably to 2024.

Professional services jobs saw a large decline in weekly nominal earnings growth in 2024. Median earnings fell by 5.8% from a high of 10% in 2023, reversing just over half of the earnings gains made in 2023. While the overall sector wages led growth in 2024, AGS category jobs lost in 2024. Slow hiring for professional service roles coupled with the large earnings increase in 2023, have rebalanced wages for these jobs in 2024. Expect earnings to rebound in 2025, but much lower than the highs of 2023.

Real wages, which refer to the purchasing power of an individual’s earnings, adjusted for inflation, grew by 1% in 2024 as annualized inflation fell to 3.2% for the year.

This growth is near identical to 2023, which grew at 1% with 4.1% annualized inflation. Real wages are still catching up to the -2% loss in 2022 during an annualized 8% inflation rate. In 2024, nominal wages grew while real wages fell slightly as prices started to rise again.

There are already warning signs that US inflation is likely to rise again in 2025. The Federal Reserve has indicated that it was moving its focus away from the labor market, back to price stability in 2025, as increases in the Consumer Price Index and Producer Price Index are signaling higher inflation. Inflation expectations are currently at their highest since 1995, due to a growing economic conflict between the US and trading partners. Inflation will be a large factor in the direction and intensity of wage growth in 2025.

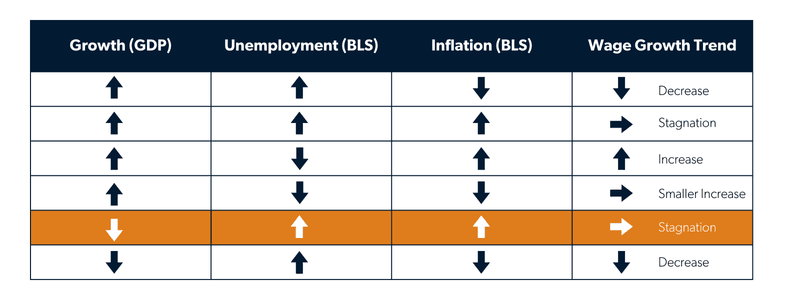

There are many different moving metrics in the labor market and economy in 2025, but wages will be determined by overall economic growth, unemployment and inflation. Below are projections of wage trends based on the three aforementioned factors:

It is likely that the US will see decreased growth from an already weakening real economy, compounded by tariffs, government spending cuts, general uncertainty and China continually gaining more market share across the world. Unemployment is likely to rise as manufacturing, healthcare, education and government sectors will have the hardest time weathering tariffs and decreased government spending.

Decreased growth would usually put a damper on wage growth, but inflation is likely to continue, as tariffs push prices onto American producers/sellers, who then pass prices onto the consumer. This would create a period of stagnation, where growth weakens, unemployment rises, but wages continue to rise with prices. In this scenario, the Federal Reserve is likely to raise interest rates to destroy demand and fight inflation, leading to weaker labor market conditions.

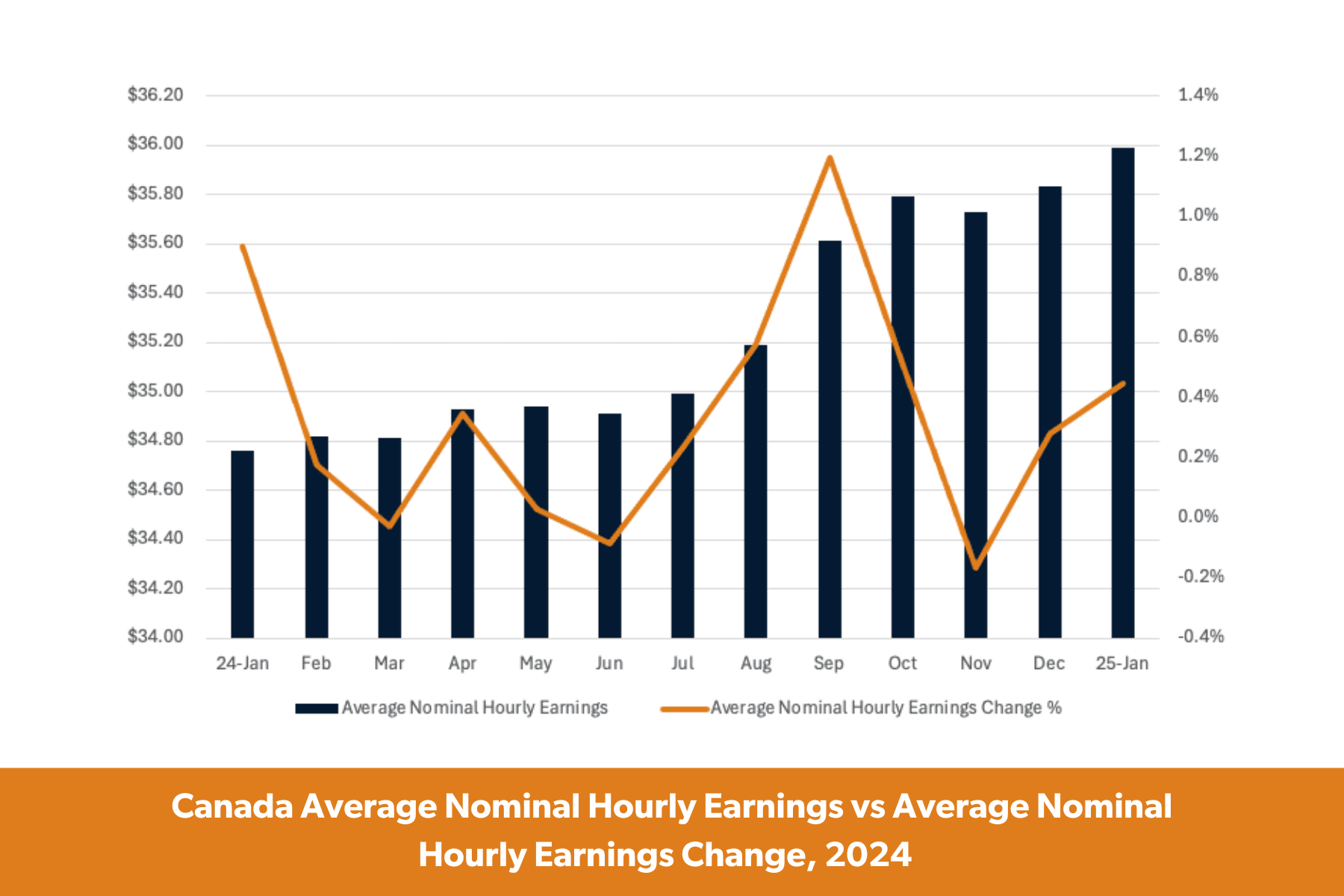

In 2024, average hourly earnings in Canada grew nominally by 1.23 CAD, or 4.4%. This growth is weaker compared to the past two years, with 2022 seeing a 4.7% average hourly earnings increase, and 2023 seeing 5.3%. Overall average hourly earnings have slowed in Canada as labor market conditions have deteriorated and overall economic growth has slowed over the course of 2024.

Sectors that led Canadian average hourly earnings growth in 2024 include natural resources, agriculture and related production at 7.9%; natural and applied sciences at 5.6%; and business, finance and administration at 5%.

Sectors that saw the least average hourly earnings growth in 2024 were arts, culture, recreation and sports, coming in at 0.6%; manufacturing and utilities at 1.7%; and sales/services at 2.5% . Wage growth was strongest in large metropolitan areas such as Montreal or Quebec City, but also was strong in smaller cities such as Windsor. Middle-of-the-country providences and remote areas saw the least amount of wage growth.

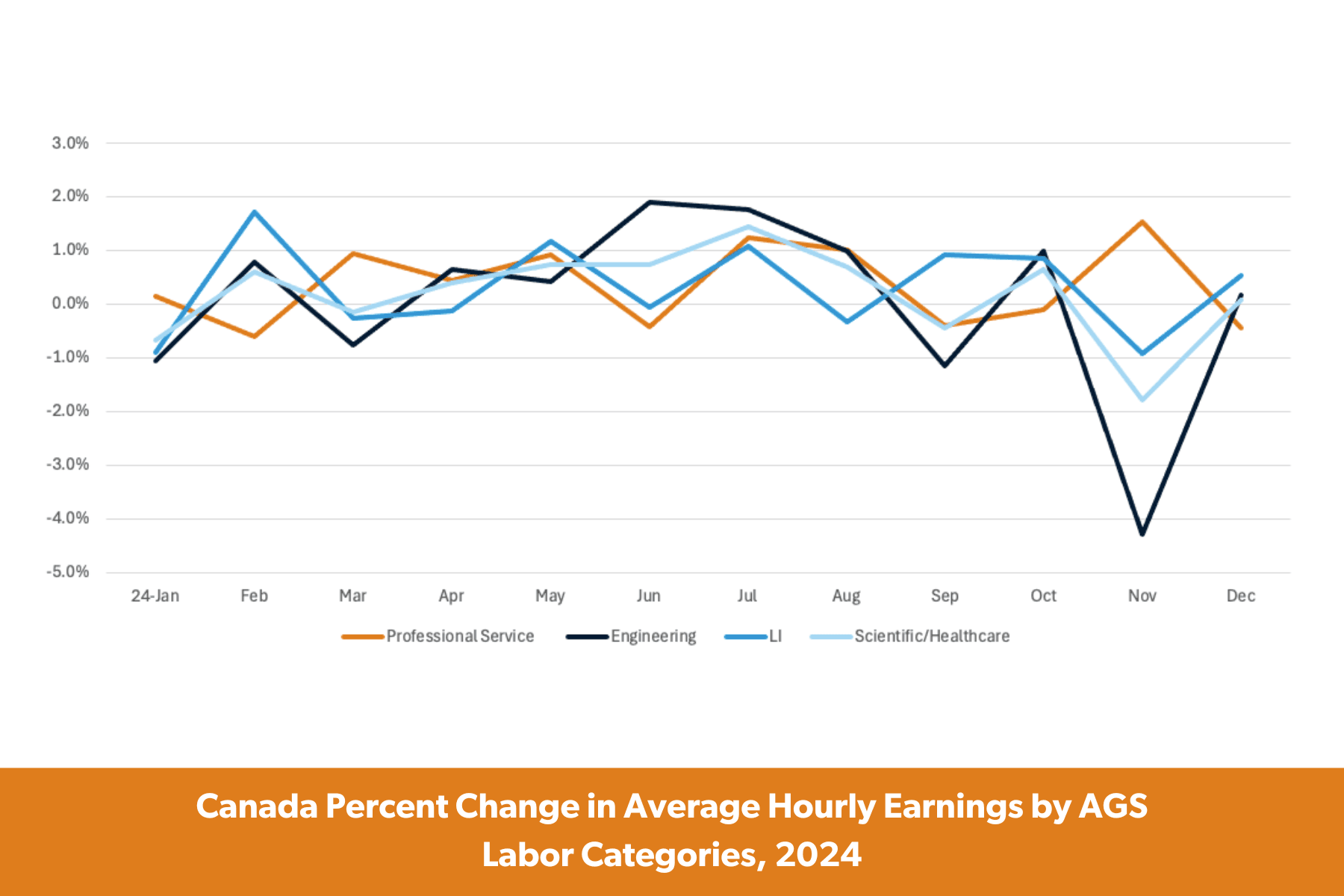

For AGS labor categories, professional service jobs had the largest average hourly earnings increase at 4.3%. This is down from a 5.2% growth rate in 2023. Much of this is led by finance/real estate and professional, scientific and technical job growth, two sectors that added jobs at a rate of 2.9% and 3.4% respectively in 2024. It appears that job growth in these sectors will continue to be strong in 2025, so expect professional services hourly earnings to grow.

Following professional services was the light industrial labor category. Hourly earnings grew at 3.8% in 2024, up from 2.1% in 2023. While the manufacturing sector lost jobs in 2024, overall, the goods producing sector is up, with stronger contributions from oil/gas and warehousing sectors. In 2025, the light industrial labor category’s wage growth could be threatened by potential tariffs from the US. Manufacturing could lose more jobs as American companies re-shore operations to reduce tariff costs, leading to weaker wage growth.

Scientific/healthcare labor category jobs saw an average hourly earnings growth of 2.4% in 2024, down from 5.2% in 2023. In 2023, Canada spent 12.1% of its total GDP on healthcare, with wages being the single largest cost in the system. Even with increased healthcare spending in 2024, wage growth dropped. Average hourly earnings growth in 2025 will likely mirror 2024.

The engineering labor category struggled in 2024 -- only achieving an average hourly earnings growth rate of 0.5%, down from a high of 7.2% in 2023. While the goods-producing sector had a relatively strong year, engineering jobs did not see that growth. This is due to the large supply of engineers in Canada as the number of engineering students has increased by 25% from 2014 to 2023. Coupled with higher immigration rates and a shrinking manufacturing sector, engineering jobs did not see much growth this year.

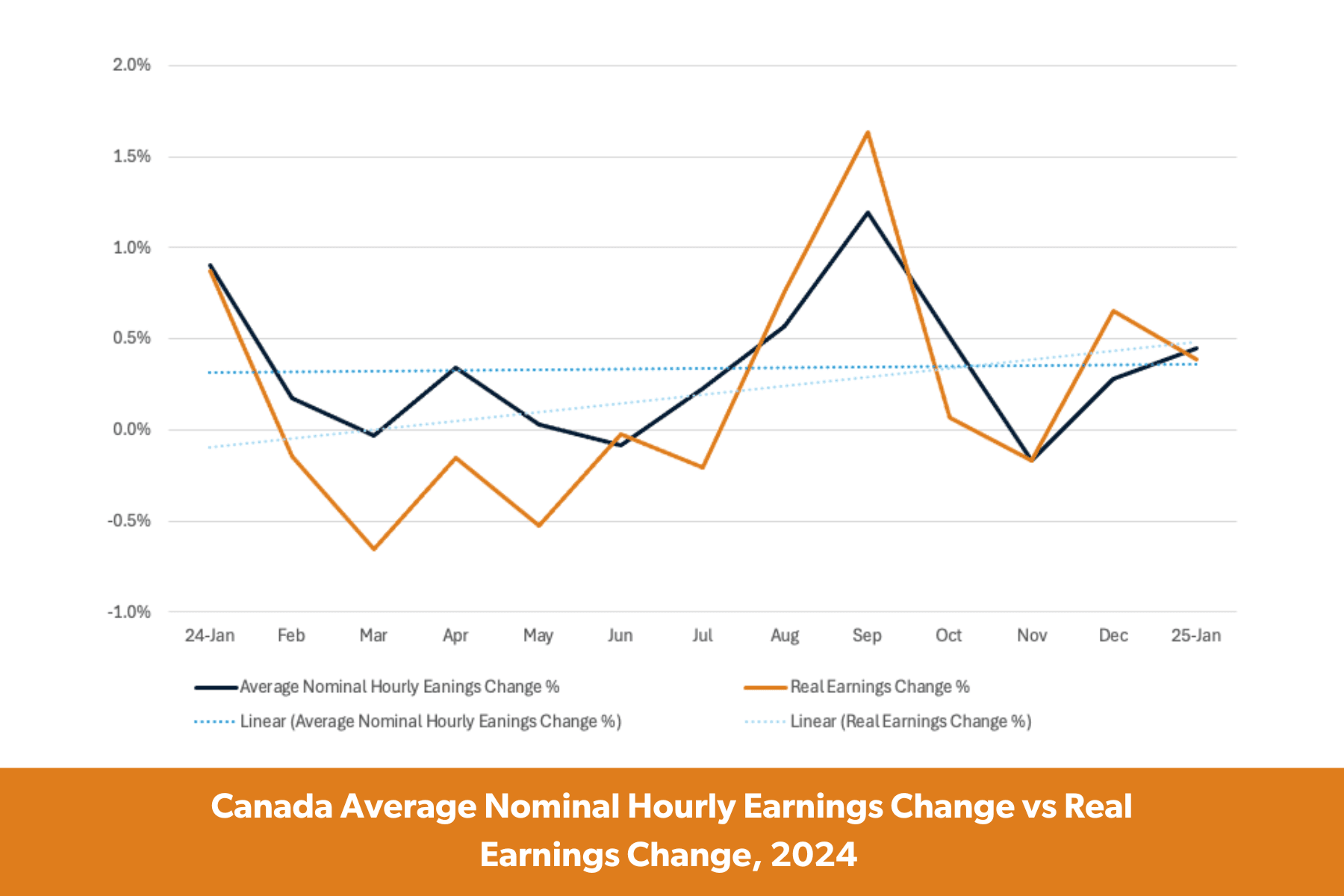

Real wages in Canada grew 2.1% in 2024, with a 2.4% annualized rate of inflation. Real wages grew last year by 2% with an annualized rate of inflation of 3.9%. Real wages decreased in 2022 by -1.4%, with a 6.8% annualized rate of inflation. Canadians have experienced real wage growth over the past two years, with consumer prices stabilizing around 2% annually. However, housing affordability remains a significant issue. Inflation could also tick up because of the economic conflict with the US. Canada is the biggest receiver of American goods, particularly motor vehicles and industrial machinery/parts. While tariffs wouldn’t have much effect on the price of food, energy or housing, they could still cause inflation for certain products, which if bad enough, could cause higher wage growth.

While there is a possibility of higher inflation for Canada in 2025, it is more likely that wage growth will slow. Inflation appears to be under control and GDP is growing, so expect wages to grow more similarly to pre-pandemic times.